CENTRAL BANKS & MARKETS UPDATE Q1 2023

Markets in 2022 were mainly characterised by central bank tightening their monetary policy, but in 2023 it looks like these hiking cycles may be coming to an end. Let’s take a look at where the major central banks are, and what that implies for the markets.

Federal Reserve

The Fed was ahead of the pack in hiking rates and initiating QT, and naturally they also seem to be ahead in terms of slowing down and eventually stopping. Chairman Powell, vice chair Brainard and other Fed members have been repeatedly stating that once a peak in rates is reached, it will stay there for a significant period of time. However, the markets still don’t seem to believe that, pricing lower rates in 2024 and driving the yield curve to very inverted levels. This tug-of-war has been going on for weeks and is ongoing, but it feels like the market is very stretched at the moment in terms of expectations from the Fed. US inflation has been dropping at a decent pace, down from over 9% YoY to 6.5% on the last CPI reading.

European Central Bank

The European Central Bank was late in starting to hike rates, and the rate of tightening has been slower than the Fed (peaking at 50bps per meeting). Inflation has rocketed higher since 2022, rising from an average of around 2% to over 10% YoY. The key difference to the US inflation figures is that the Eurozone inflation is dropping at a much slower pace. This is primarily due to the Eurozone’s strong dependence on imported energy; this factor has kept price pressures high and is expected to continue to do so. Chair Christine Lagarde and many other ECB members remain hawkish, projecting more 50bp hikes for as long as inflation stays above target.

Bank of England

Unsurprisingly, it’s a similar story in the UK in terms of inflation. CPI shot higher in 2022, reaching a YoY peak above 11% and still printing over 10%. The BoE has a difficult task in its hands, trying to fight inflation with tighter monetary conditions while the UK economy shows increasing signs of an incoming recession. This has been reflected in some of the MPC members, having two voting for no change in rates, in the last interest rate decision meeting. The Bank of England is arguably one of the most dovish central banks, and this can put downward pressure on UK rates and Sterling.

Bank of Japan

Japan has enjoyed very low inflation for decades, and this has enabled it to run an extremely accommodative monetary policy for a prolonged period. Inflation has finally started to substantially exceed their target, and this has led the market to finally price a BoJ move away from negative rates. There was growing expectation for a change in policy in this week’s rate decision meeting, but that didn’t materialize, much to the JPY bulls’ frustration. The markets are certainly pricing a change in BoJ policy, with the Yen having appreciated over 15% vs. the USD in the past 3 months.

Market Implications

The main driver for markets has arguable been the level of yields, with the 10y US Treasuries in particular. As mentioned above, the curve has remained very inverted in the past months, and this phenomenon almost always precedes a recession. It’s probably fair to say that the market is pricing too much easing too quickly for the Fed, and so a bounce back in yields is possible in the short term. We have bounced from a confluence of supports in the US 10y yield, and a potential rally could have targets in the 3.60s or even challenge the previous highs at 3.90%.

If yields move higher from here, then the logical reaction would be to see the US Dollar strengthen. With support confluence in the low 102s, we could rise towards the next upside targets at around 105 and 108.8

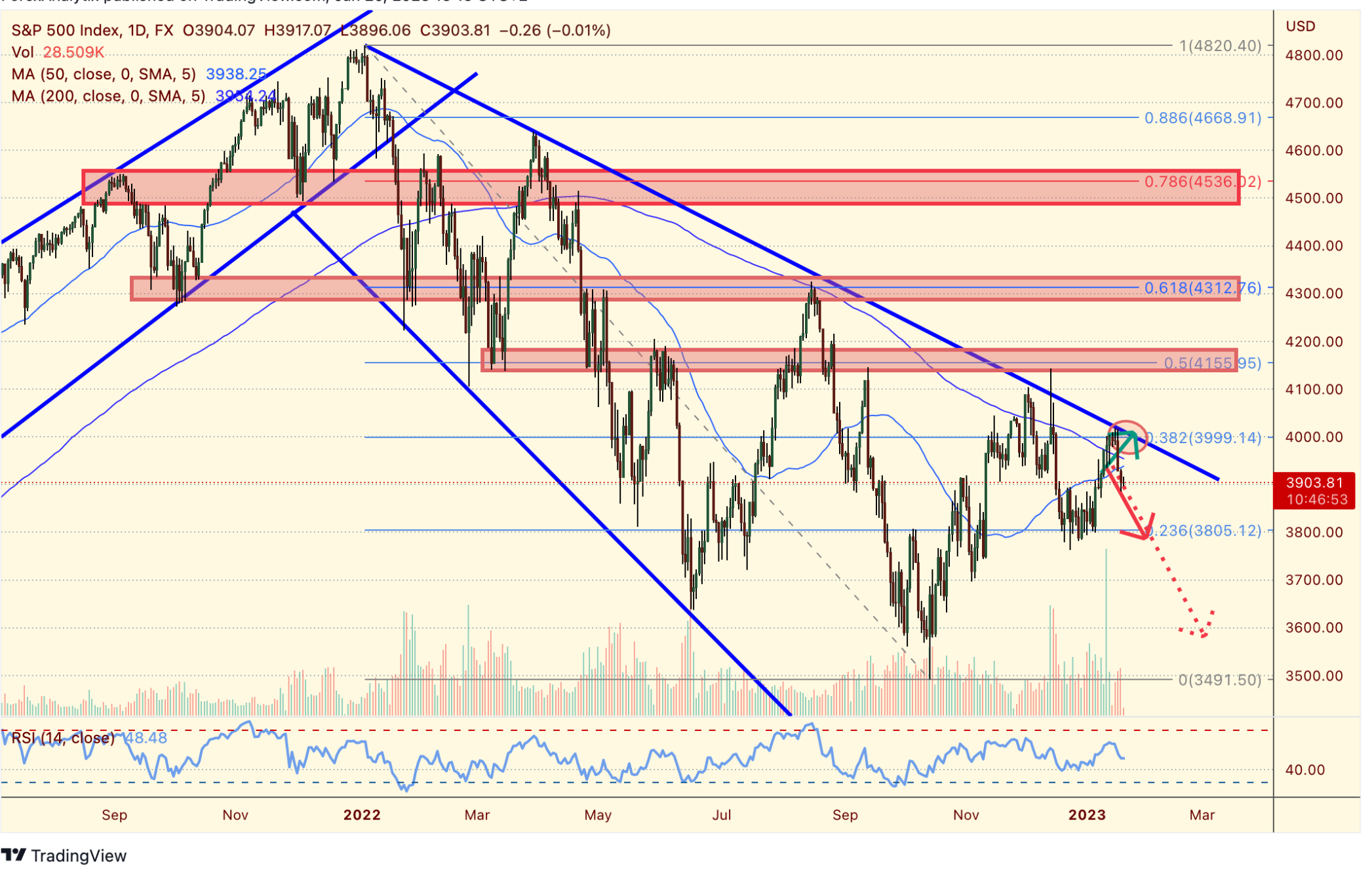

Equities have been quite resilient in the face of rising yields, but the global economic environment has turned for the worse in the past few months. The S&P500 index has already dropped nearly 20% from the all-time highs, but there is still potential for more downside.

Since 2008, the market has been conditioned to get into buy-the-dip mode as soon as the economy weakens, anticipating supportive central bank action. However, the current environment might finally be marking a change to this behaviour. The combination of higher yields, high inflation and a fall in general company earnings might be the catalyst for another leg lower in risk assets. The S&P500 index – currently at around 3900 points – has important resistance at around 4000, and a potential downside at around 3600.

The main takeaway from all the above is that there is currently an apparent central bank divergence, and this may persist in the near term:

- the ECB is hawkish and still behind on the hiking cycle.

- the Fed is hawkish but near the end of the hiking cycle.

- the BoE is dovish and near the end of the hiking cycle.

- the BoJ is still dovish but should embark on a hiking cycle soon.