The perfect inflation storm

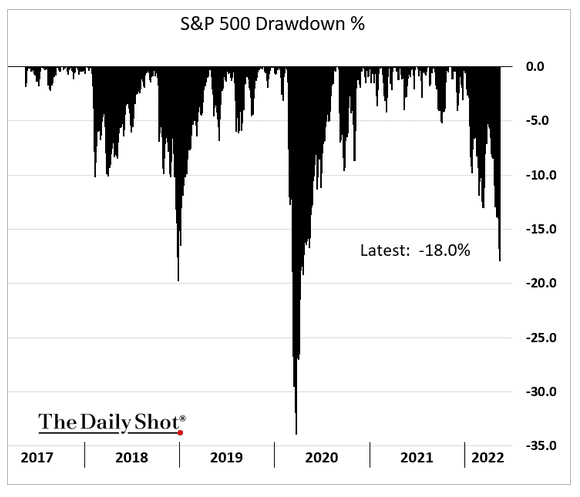

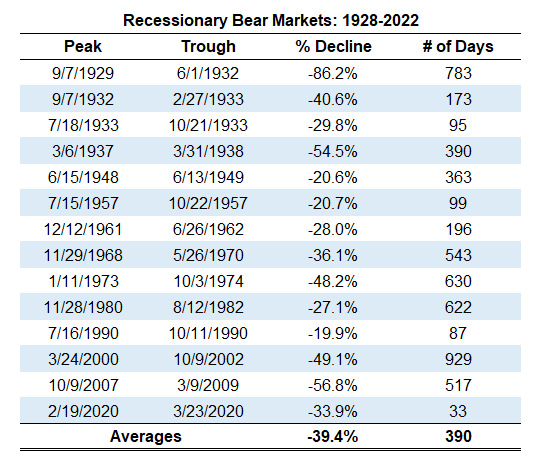

In the past six weeks, shares have fallen every week. This has not been the case since mid-2008. It is only that the S&P 500 recovered last Friday, otherwise it would have lost more than 20 percent from its peak last year, the point at which there is a formal bear market. More than 4,000 US stocks fell to their lowest point in 12 months last week. The average share is even 40 percent below the top.

There are several reasons for this decline.

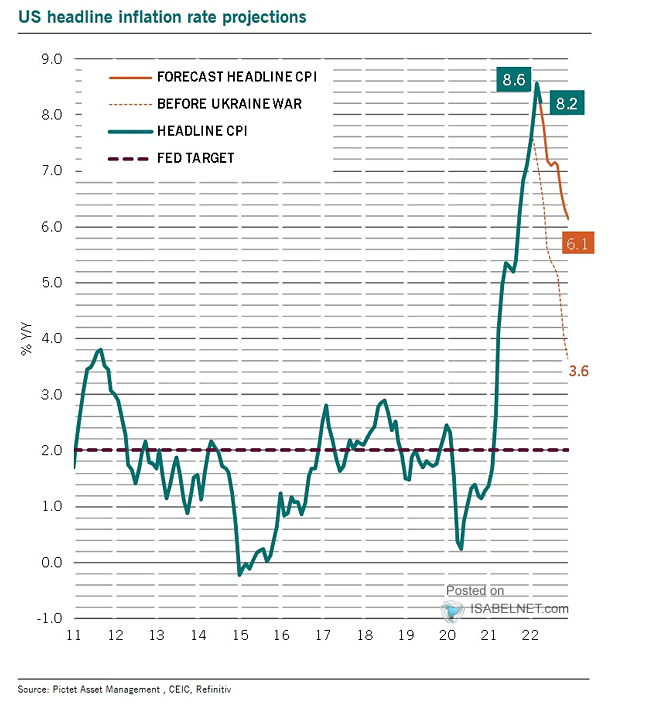

It started with the turn in monetary policy in the United States, the moment when the narrative of ‘temporary inflation’ turned into ‘persistent inflation. After last week’s US inflation data, there appears to be plateauing rather than a recent spike in inflation. Inflation is also increasingly spreading in the economy, not only in products but also in services. However, there is a widening gap between Core CPI (5.7 percent) and Core PCE (3.3 percent). This does not make communication from the Fed any easier. The PPI figures show that there is still plenty of inflation in the pipeline. When the March and April figures are added together, there is no two-month period in US history when producer prices have risen so rapidly.

The only way to curb inflation is to slow down economic activity. Apart from the Bank of Japan and the People’s Bank of China, central banks are now doing this. The market now seems to be more afraid of the slowdown than of high inflation. The market still seems to underestimate long-term inflation. This fear of a slowdown is also fuelled by the Fed’s statement that, instead of the intended soft landing, it could at most be a ‘not so soft’ landing (softish). On the one hand, Powell is thus indicating that he is prepared to hurt the economy, but on the other, he would also prefer to see a lower stock market. After all, the consequence of a somewhat more complex landing on the economy is that company results come under pressure. Whereas US equities corrected mainly based on valuation until mid-April, there has hardly been a correction based on deteriorating earnings prospects.

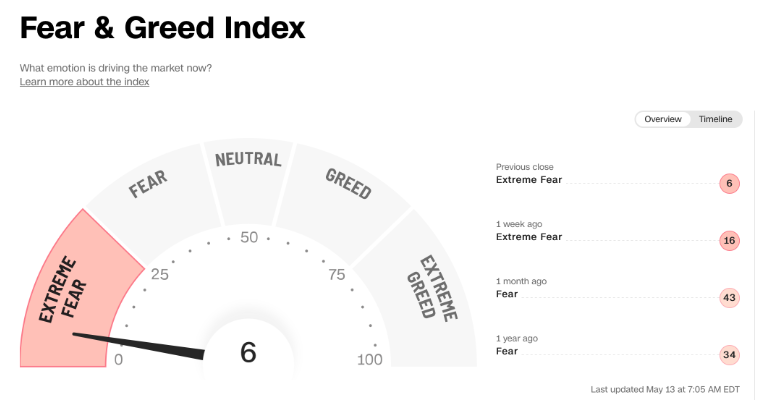

In addition to inflation, monetary policy, and the slowdown in growth, the stock market has of course not been helped by the war in Ukraine and the lockdowns in China. That has also helped push prices down. Some investors dare to buy sharply lower stocks, under the motto that all the bad news is discounted in the price, and given the recent deterioration in sentiment (see, for example, the Fear & Greed indicator), a bear market rally after six weeks of decline is quite possible.

In November, the S&P 500 was still valued at 21.5 times earnings. This has now fallen to a perfectly reasonable 17 times earnings, but it is the earnings that are now being called into question. Moreover, the rise in interest rates has caused the risk premium on shares to fall rather than rise. The first-quarter figures were still fine, but expectations for the second quarter have been lowered, while those for the whole year have remained the same. This means that more has to come out of the second half of the year when there is a slowdown in growth, not a good combination. To compensate for this, the S&P 500 should now rather be at 14 to 15 times earnings. The only question is whether the market will take the worsening earnings outlook into account now, or only when it is formally confirmed by the companies.

In addition to lower profit margins, there is also the issue of inflation in the somewhat longer term. The market seems to assume that 80 to 90 percent of interest rate increases have already been discounted. Many interest rate rises have indeed been priced in, but, remarkably, the expected peak in interest rates will not be higher than inflation. This is even though a positive real interest rate is required to slow down the economy. Even though Powell wants to come across as Volcker, there is still a chance that if inflation levels fall a little in the second half of the year, the Fed will declare that monetary measures are effective and that it can ease policy a little. This could lead to a rally in equities, but at the same time, it would leave us with relatively high inflation for much longer.

In the end, it all comes down to inflation expectations. In that respect, unfortunately, there is a perfect storm. Many long-term structural factors are causing inflation to rise this decade. For example, the ageing of the population is causing more inflation. People who for years worked one day a week for their pensions are now going to consume that amount, while they no longer contribute to the economy. That is inflationary by definition. The comparison with Japan is often quoted, but the structural deflation there was mainly a consequence of the bursting of the double bubble in the early 1990s, not of ageing. Another structural factor is deglobalisation or regionalisation, something that increased in the world after the Russian invasion. In addition to globalisation, telecommunications and IT have also depressed prices in the past. Most IT companies have now become monopolists due to their disruptive innovation, not a market form known for falling prices. There is also a clear social movement away from the capital-labour pendulum and towards the labour factor. Perhaps under pressure from social media and aided by the tight labour market, employees can demand a larger share of the profits. This depresses profits and creates the dreaded wage-price spiral. Another structural factor causing more inflation is the changed monetary policy to solve the high debt mountain. Whereas before the Great Financial Crisis (GFC) the policy was aimed at less inflation, now it is more inflation (financial repression/reflation). After all, debt is always expressed in nominal GDP. More inflation helps to reduce debt as a percentage of income. Furthermore, the post-GFC and certainly post-Corona policy has become much more Keynesian, with a greater role for government with many investment programmes, actually financed by the central bank and, on balance, more inflation.

On top of these structural factors that lead to higher inflation, there is the tactical monetary and fiscal policy that is now causing more inflation. In a short time, the money supply has increased by 30 percent and, as inflation is primarily a monetary phenomenon, we are now seeing the downside. In the short term, this 30 percent demand impulse has also caused problems in supply chains and the consequent overheating of the economy. Finally, there is the war in Ukraine. Not only do wars always cause more inflation, but the fact that this causes an oil shock and also a shock in food prices (1 in 8 calories in the world comes from Ukraine and Russia) completes the picture of the perfect inflationary storm. It is virtually impossible to reverse this with the Fed’s currently intended policy. The Fed will have to inflict more pain on the economy and thus the market.

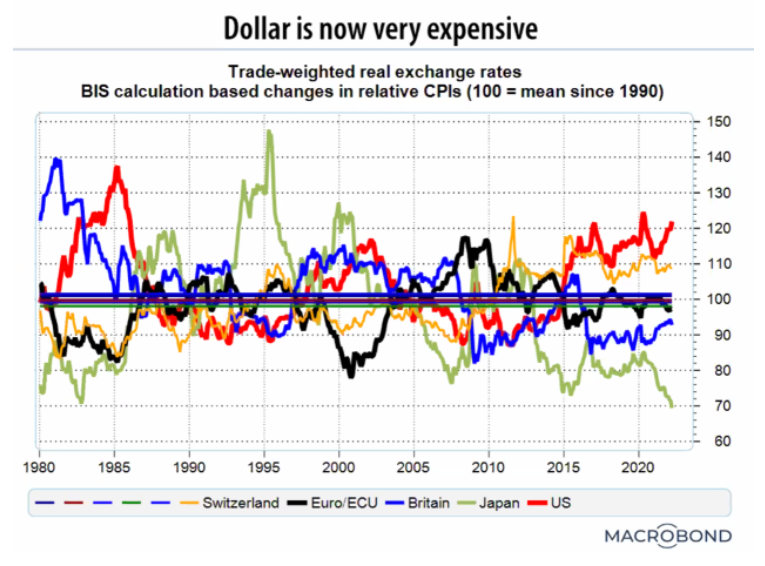

The result is, foremost, that more air will run out of the bond market. The past few months have been fast; the sequel will be more gradual. Higher interest rates and inflation make US equities relatively expensive, also because equities outside the US were already cheap before. When we talk about the stock market these days, we are talking about US equities because two-thirds of the total stock market consists of US companies and many stock markets outside the US are strongly correlated with the US stock market. That is the characteristic of expensive shares, they have a heavy weighting in the index. So there will be a further rotation from the more speculative sectors too, for example, energy, mining, agricultural companies, forestry, etc. These stocks have already risen sharply recently, making it difficult for many investors to buy them now, but valuation and fundamentals justify another doubling. The time is also approaching when Chinese equities and emerging market commodity stocks will outperform those of countries where monetary madness has struck. The dollar is still the safe haven, but will weaken in the long term, especially against Asian currencies.