Buy the rumour, sell the news

The attack on Iran has shaken the financial markets. The reaction was predictable: oil and gold prices rose, while shares came under pressure. Social media and news sites are full of scenarios about oil prices peaking at $100 per barrel and economic chaos. Now is actually a good time to sell oil and gold and buy shares that are being dragged down by the decline.

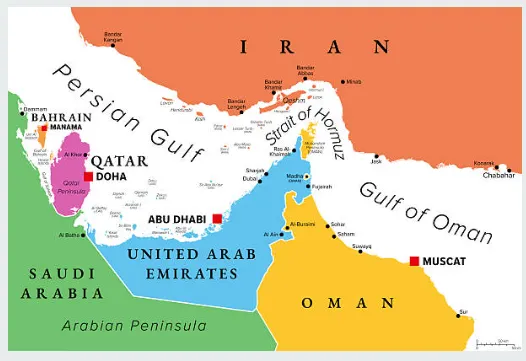

The Strait of Hormuz is central to investors’ perception of risk. More than fourteen million barrels of oil pass through this strategic sea channel every day, ninety per cent of which is destined for Asian buyers. Iran has threatened to block this channel in the past, but an actual closure would also be strongly contrary to its own economic interests: it would also block its own oil exports and currency revenues. Moreover, Iran’s navy, or what remains of it, does not appear strong enough to sustain a prolonged blockade. De facto, the Strait is already largely out of use due to increased insurance premiums and advice from the US Navy to avoid the route, but this is a temporary effect.

What the market seems to be underestimating is the extent to which military and political relations were already priced in before the operation began. Oil and gold have each risen by around 20% since the beginning of 2026, coinciding with the build-up of US military capacity in the region. The classic Wall Street adage “buy the rumour, sell the news” applies here. Now that military action has actually taken place, the uncertainty premium that had been priced in for weeks is disappearing.

The geopolitical situation in Iran itself also plays a role. The death of Supreme Leader Khamenei, the formation of an interim council, and increasing internal pressure from possible popular uprisings are creating a regime that is interested in reaching an agreement quickly. Even before the attack, the Iranian Foreign Minister indicated that his country was close to a nuclear agreement. Under the current circumstances, the incentives for de-escalation have become considerably greater, not smaller. President Trump has signalled his openness to negotiations, and neighbouring countries such as Saudi Arabia, which have themselves been attacked by Iranian missiles, also have an interest in seeing tensions ease quickly.

China is Iran’s most important oil customer, and Beijing has an obvious interest in the unimpeded flow of traffic through the Strait of Hormuz. A prolonged closure would directly affect the Chinese economy, thereby increasing diplomatic pressure on Iran from that quarter. This reduces the likelihood of an escalation that would structurally disrupt the oil market.

That does not mean that all risks have been eliminated. The Revolutionary Guard, Hamas, Hezbollah and the Houthis operate partly autonomously and may act in an escalatory manner, even if the Iranian interim government seeks de-escalation. Damage to oil facilities in the region or to tankers in the Red Sea remains a real risk.

The logical investment strategy here is to sell oil and gold if they continue to rise on the initial shock, and to buy equities, particularly those related to tourism, if they come under pressure. Tourism is currently being temporarily affected by cancelled flights and travel advisories, but this will quickly recover as soon as signs of de-escalation emerge. Historically, situations in which the market overreacts to temporary geopolitical shocks have offered good entry points.

The base scenario remains that most of the relevant parties — Iran, the US, Israel, neighbouring Arab countries and China — have a common interest in bringing the hostilities to a swift end.

The military campaign is therefore not the start of a regional war, but rather the escalation that will enable de-escalation. Markets like clarity, and as soon as that clarity emerges through negotiations, fear-driven positions in oil and gold will quickly unwind.

A frequently heard hope is that Operation Epic Fury will trigger a fundamental regime change in Iran. That expectation deserves some nuance. The Revolutionary Guard is not just a military organisation; it is deeply intertwined with the Iranian economy through an extensive network of companies, construction consortia and trading houses worth tens of billions of dollars. Eliminating individual leaders will do little to change this: the Revolutionary Guard has a strict hierarchical system in which every fallen commander has a successor trained in the same system. Regime change from outside is, therefore, an illusion; the structure is more robust than the individuals who lead it.

If, nevertheless, history were to take a surprising turn and regime change were to occur, it might be the best thing that could happen to Iran, the Middle East and the world. Iran has traditionally been a civilised, prosperous and remarkably pro-American country with a highly educated population, a rich culture and enormous natural resources. Under a government that no longer funnels billions to foreign proxies, nuclear ambitions and internal repression, but invests in its own economy and citizens, Iran could rapidly develop into a regional economic powerhouse. For the Middle East, the disappearance of the main financier of destabilisation would offer a historic opportunity for lasting peace. And for the world, an integrated Iran means more oil on the market, lower energy prices and a region that is finally realising its economic potential. It is a scenario that few dare to voice, but which almost everyone quietly hopes for.

In the meantime, do not be swayed by the headlines. Volatility is the price you pay for returns. Those who sell now out of fear usually miss out on the recovery that follows. And those who calmly respond to temporary dislocations position themselves for the recovery that is almost certain to follow once the fog of war lifts.

{kind=link}